If your plans for a multibillion-dollar data center are on hold while you wait for electrical power from the grid, you’re not just losing time, you’re losing revenue and market share. That’s why data center developers and hyperscalers are not waiting — they’re moving fast.

“Energy dominance is extremely important to AI dominance,” Bloom Energy CEO KR Sridhar said in a conversation with Maria Bartiromo during the World Economic Forum. “People are migrating to where the power is.”

The century-old power grid system was not built for the digital age. And the strain is showing. It can take years for utilities to supply new data centers with the power they need. Today, the primary limiting factor for data center growth is time to power.

Companies moving at the speed of AI require power at the speed of AI, and they are increasingly taking matters into their own hands, Bloom Energy’s 2026 Data Center Power Report reveals. They are choosing new geographies where time to power is shorter and bringing in onsite power to meet their needs.

These massive changes are happening at breakneck speed. In two years — by 2028 — the energy market is expected to look radically different: New geographies. New high-voltage and DC architectures within data centers. And many more data centers running off-grid, using entirely onsite power.

It’s going to be a whole new world.

Demand for power is driving change

McKinsey and Company predicts that the total power load of data centers will nearly double in just three years, from 82 gigawatts in 2025 to 153 GW in 2028, driven almost entirely by growth in AI workloads. That’s twice the growth rate predicted just one year ago.

With this fierce demand for power, Bloom’s Power Report found that data center leaders are concentrating their growth plans on a small number of top hubs, expanding existing campuses, and adding new locations where they have the greatest ability to get power on the timelines they need.

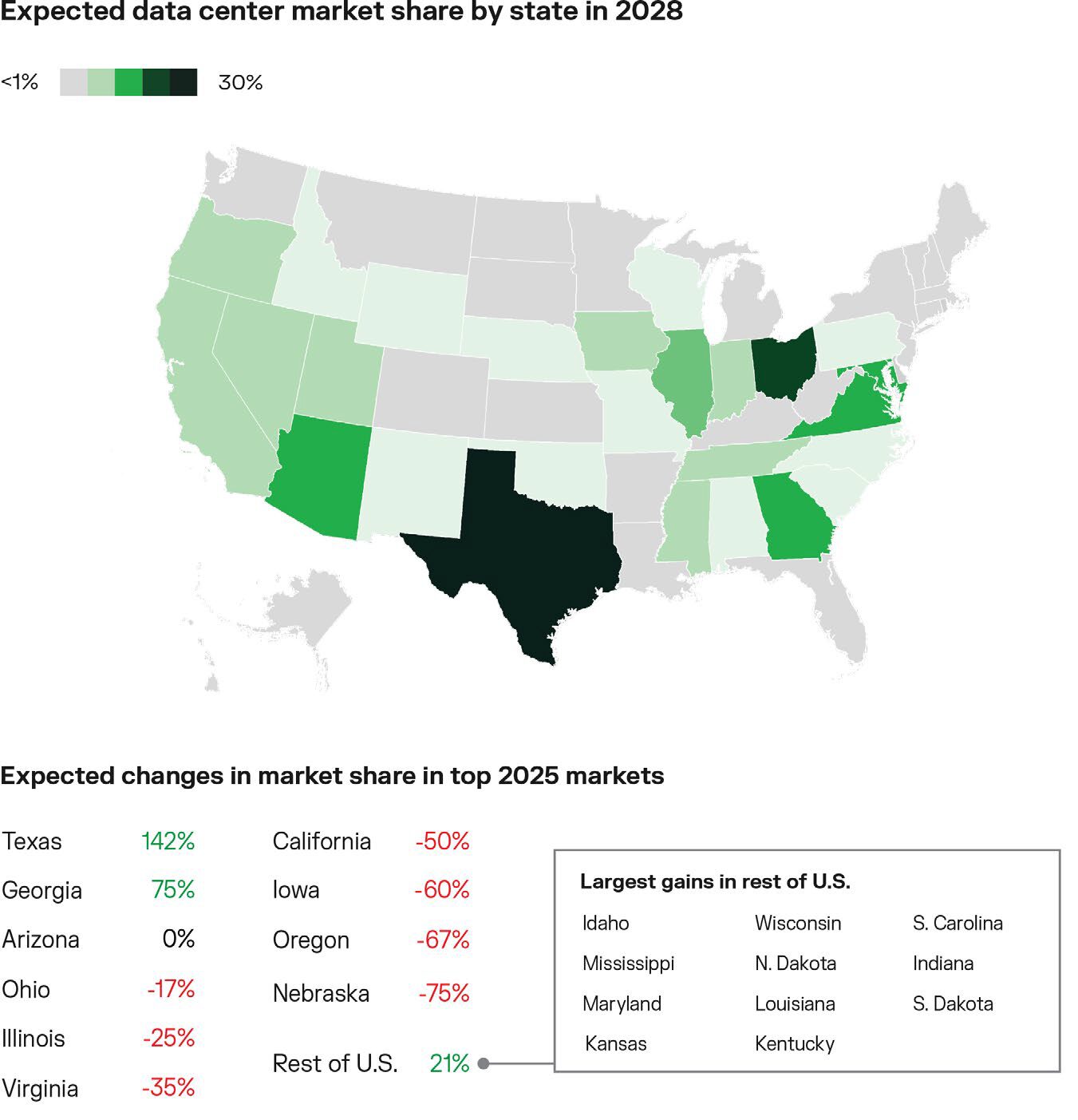

“All this demand will be concentrated in regions where power is an advantage today, and that is primarily Texas and the Southeast. Those are states where a lot of land, power, and gas are available,” says Bala Naidu, VP of Energy Transition Solutions at Bloom Energy. “A lot of the traditional legacy data center markets will lose market share in the process.”

That will lead to dramatic changes in the geography of U.S. data center distribution. The following states are expected to see significant market share changes by 2028 compared to their positions in 2025:

- Texas +142%

- Georgia +75%

- Arizona 0%

- Ohio –17%

- Illinois –25%

- Virginia –35%

- California –50%

- Iowa –60%

- Oregon –67%

- Nebraska –75%

Source: DC Byte analysis as of Oct. ‘25, including 50 states and the District of Columbia

In short, data centers will move to states where they have great conditions: access to natural gas, rapid and simple permitting, and access to water. And when they need to, they’ll install onsite power rather than wait for the grid.

Hyperscalers and colocation providers responding to Bloom’s survey reported that they expect to be able to get grid power for their data centers within a year or two. Utilities, however, gave timelines that are 1.5 to 2 years longer, with their timelines varying by region.

In the legacy markets, time to power is simply too long. The lack of overall power availability, interconnection delays, permitting red tape, and other utility- and regulator-based delays are adding up, and that will cost them valuable market share.

New data centers, new architectures

The next two years will also hold startling changes in the design of data centers themselves.

An increasing number of data centers will require a gigawatt or more of power. That’s as much electricity as a mid-size city, like San Francisco, consumes at its peak. By 2030, one-fifth of data centers are predicted to be gigawatt scale, and by 2035, it will be one-third.

“That’s a dramatic shift that is going to drive changes in how people design these sites,” says Naidu.

Driven by the need to support racks with higher densities than ever, data center leaders are moving toward new, more efficient power architectures.

These next-generation electrical designs, with high-voltage busways (over 480 volts) and direct current (DC) architectures, can deliver higher power density, greater efficiency, and faster deployment.

- A strong majority (60%) of respondents to the Power Report say they will be using high-voltage busways by 2028.

- Additionally, almost half (45%) say they’ll be using direct current (DC) architectures by 2028.

- After 2030, all of the respondents — 100% — predicted that their data centers would be using both high-voltage and DC architectures.

Urgency drives onsite power expansion

With gigawatt campuses and new power architectures on the way, it’s no surprise that data center developers are increasingly looking to onsite power generation to meet their needs.

But it might be surprising to learn that one-third of hyperscalers and colocation providers expect to be operating data centers that are powered entirely by onsite power by 2030.

This indicates that onsite power is no longer a temporary “bridge” until grid power is available, nor is it merely a backup power solution. Onsite power is rapidly becoming a permanent pillar of data center planning and a trusted source of primary power.

“Ever since we started this survey, we have seen a 33-fold increase in the number of people who think onsite power is going to become the norm,” Naidu says. And, he adds, nearly half of those are considering fuel cell technologies for generating that onsite power.

This year’s Data Center Power Report makes it clear: Driven by the need to remain competitive, hyperscalers and colocation providers are not waiting. They are moving rapidly to reshape the way they build data centers — and the way they get power to them.

The next two to four years will be transformative. In this landscape, the hyperscalers and data center developers moving to onsite power aren’t slowing down — they’re moving faster than ever to adopt new architectures, move into new geographies, and install more onsite power.

To get the full details, download Bloom Energy’s 2026 Data Center Power Report for free.