Summary

Two major trends in California’s electric market are creating an uncertain financial outlook for investor- owned electric utilities (IOUs) that serve approximately 58% of California’s electricity.1 The first is the proliferation of Community Choice Aggregators (CCAs) and “direct access” (DA), shrinking the amount of electric generation IOUs serve, and eroding a significant portion of their revenue as a result. Customers who continue to take “bundled” service – receiving both delivery and generation from the IOU – are bearing the cost of this lost revenue from customers opting to take “unbundled” service through one of these alternate channels, but regulators are beginning to address this imbalance by increasing charges for “unbundled” customers. The second transformative trend is the increasing occurrence of devastating wildfires, the response to which is triggering unprecedented levels of new investments and increased operating expenses that are sure to lead to higher consumer electric rates. The staggering financial liabilities and future mitigation costs will weigh on both bundled and unbundled customers, and create a high degree of uncertainty over future cost structures for utilities. This uncertainty and increasing financial instability is a new normal for an industry traditionally considered highly stable.

Customer Choice in California

Background

In the late 1990s, California followed a trend that was sweeping the country – deregulating its electric market and allowing customers to purchase electric supply from sources other than the IOU. However, a flawed market design and willful manipulation by bad actors led to tremendous volatility in the wholesale market, ultimately causing the skyrocketing consumer prices, utility liabilities, and grid instability that characterized the California Energy Crisis. The crisis brought deregulation efforts to a halt, and by January 2003, utilities had resumed procuring electric generation for the vast majority of customers.

Following the crisis, the state legislature and California Public Utilities Commission (CPUC) directed the IOUs to ensure they had adequate generation supply under contract to serve all customers at any given time, a requirement known as “resource adequacy” (RA). The California state legislature passed AB 57 around the same time, providing IOUs greater certainty by allowing them to collect the revenue needed for generation from new power plants through consumer rates. These actions led to a boom in construction of both utility-owned and third-party-owned power plants, where the long-term nature of the new procurement rules acted as a hedge against short-term market volatility, while also providing capacity to serve the new resource adequacy requirements. The final rules left a few, limited avenues open for IOU customers to unbundle their electric generation services. Today, the fastest growing of those channels is Community Choice Aggregators, defined as:

“Any city, county, or combination who have elected to join together to buy electricity on behalf of its residents, businesses, and municipal facilities.”2

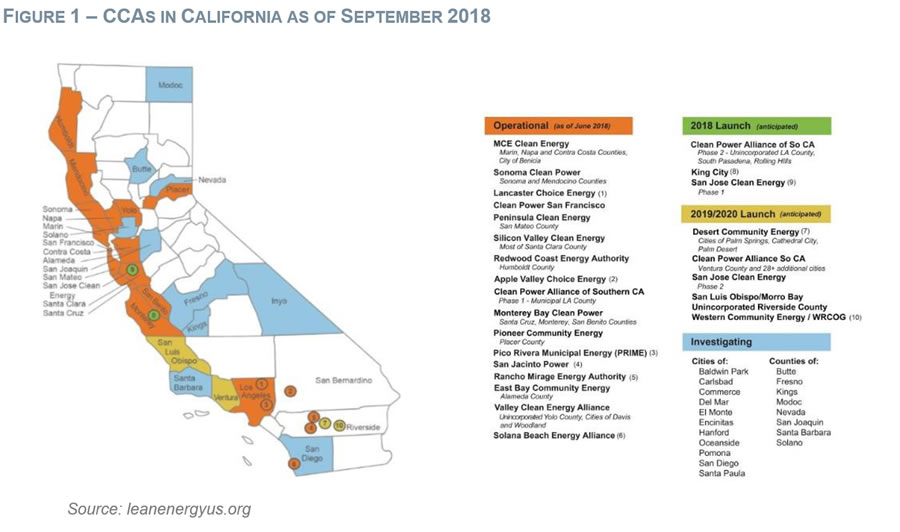

Since their introduction in the aftermath of the crisis, CCAs have grown to be a significant provider of electricity throughout the state. In 2016, CCAs provided 5,247 GWhs of electricity3, and in 2018 CCAs are projected to serve as much as 32,545 GWhs, approximately 7% of all load in California.4 Typically positioning themselves as cheaper and cleaner than the IOU alternative, CCAs are investing heavily in California renewable electricity projects, with over 2,100 MWs of capacity under construction as of August 2018.5 Lawmakers also recently expanded the second source of unbundled electricity service – Direct Access (DA) – by passing AB 237 to allow more customers to participate in a competitive market for power supply from non-utility providers. AB 237 also requires regulators to make recommendations to the Legislature on further increases in DA transactions by June 2020. Taken together, this recent activity is providing customers with growing choices for their electricity generation service.

The Growing Pressure on Utilities

During their recent period of rapid growth, CCA/DA providers have secured and maintained customers by offering consistently lower electric generation rates than offered by the IOUs. Several factors contribute to this price advantage:

- CCAs and DA suppliers benefit from the declining cost of renewable resources.

IOUs carry generation contracts dating back to the early days of renewable development, when prices were exponentially higher than those secured over the last several years. Ironically, the mandated renewable portfolio standard (RPS) requirements that forced the IOUs to acquire those contracts were a major driver of subsequent renewable cost reductions. - IOUs have to procure more generation than they need.

Each IOU must act as the “provider of last resort” for any customer in its service territory, even if the customer has opted out of their generation service. This requires the IOU to plan for changes in customer choice and load variation. - IOUs are pressured to procure resources that no other provider wants to buy.

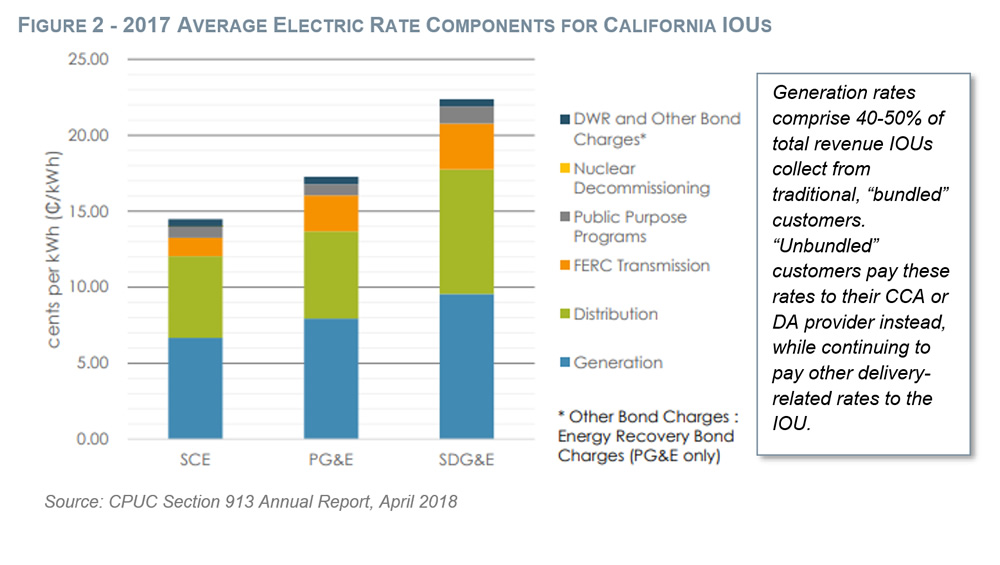

IOUs were required to sell off of a significant portion of their generation portfolio prior to generation deregulation. Today, the vast majority of utilities’ portfolios take the form of non- income-earning Power Purchase Agreements (PPAs), which have led to a larger and growing portion of grid stability and resiliency obligation costs passed through to bundled customers.6

Due to these factors, customer choice has led to higher bills for customers remaining on IOU bundled service, while unbundled have benefited from lower overall rates.7 The IOUs essentially face a “perfect storm” of upward pressure on rates—they are left holding long-term power purchase obligations, with a dwindling revenue base of bundled customers to pay for those costs. To compensate for this unsustainable market condition, regulators are beginning to increase charges on unbundled CCA and DA customers.

Regulators Stepping In

In 2017 and 2018, state regulators and legislators initiated major steps to address how IOUs will be compensated for the billions of stranded, above-market, long-term PPAs that must be allocated between bundled and unbundled customers. The challenge is to balance the RPS costs and reliability mandates, which are currently unequally weighted toward customers who remain bundled IOU customers. The CPUC is working to complete the Power Charge Indifference Adjustment (PCIA) Order Instituting Rulemaking (OIR)8. The PCIA, also commonly referred to as a departing load charge, is defined as:

“[a] correction that ensures that customers who purchase electricity generation from non- [utility] suppliers pay their share of the generation costs required to serve them. The adjustment includes costs prior to the customers’ departures, unless they are otherwise exempt.”9

The ability of non-utility electricity suppliers to continue providing lower-cost options than IOUs will heavily depend on the implementation of Phase I of this proceeding, and on the policies set in Phase II. Recent signals from the CPUC indicate that near-term departing load charges will be shifted to CCA and DA customers, and away from IOU bundled customers. In its recent adoption of Phase I of the PCIA OIR, the CPUC stated that its intention is to ensure:

“…that customers remaining on bundled IOU utility [service]…will not be required to pay costs the utility incurred on behalf of customers who left the utility to become customers of a CCA or Direct Access provider—and that departing customers do not take on costs that were not incurred on their behalf.”10

Phase II, in short, will follow this guidance to determine power procurement requirements for CCAs and DA providers, and to optimize portfolios of long-term generation contracts to support customer choice.

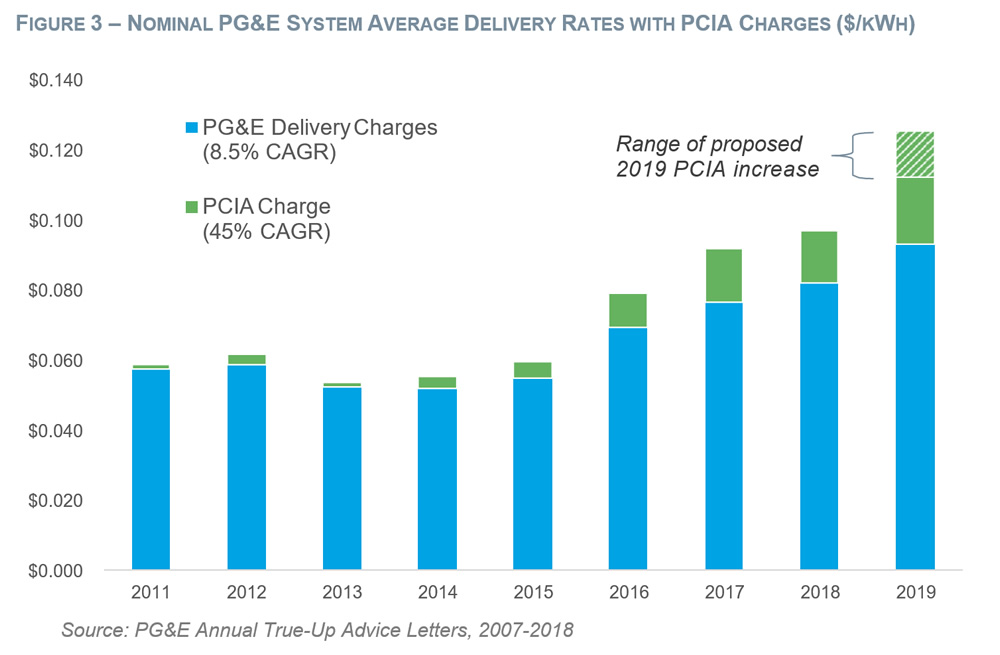

In 2019, customers will see the first major impact from these proceedings. PG&E’s November 2018 Energy Resource Recovery Account requests a 25-30% overall increase in the PCIA for all rate groups from its June 2018 rates, with increases for commercial customers potentially as high as 58%, a roughly 1 cent hike.11 The CPUC’s Proposed Decision, scheduled for a vote in early 2019, recommends only a minor 2.3% reduction to PG&E’s request12, demonstrating the CPUC’s willingness to shift the cost burden to CCA and DA customers. Regulators are expected to adopt similar rate adjustments proposed by SCE and SDG&E in early 2019.

SB 100 and the Impact of the RPS

California’s newly implemented, aggressive RPS is an additional source of financial pressure for CCAs and IOUs alike. SB 350 and its successor SB 100 mandate a 60% RPS by 2030, including interim annual RPS targets with three-year compliance periods. It also states that 65% of RPS compliance must be derived through long-term contracts of ten or more years. SB 100 requires that zero-carbon resources supply 100% of retail electricity sales to California end-use customers, and 100% of electricity procured to serve all state agencies by December 31, 2045.13 Compliance with California’s renewable goals will have little near-term impact on IOU generation rates due to the volume of long-term renewable PPAs that IOUs hold, which, thanks to relatively flat load growth and increasing departing load, already cover a significant portion of IOU obligations. However, CCAs, DA providers, and POUs (publicly owned utilities) will need to execute new contracts in order to meet long-term procurement requirements, especially those forecasting load growth.

What to Expect Going Forward

The legislature and CPUC face significant challenges balancing their mission to ensure affordable, safe and reliable service against state mandates to promote clean energy, and the steadily increasing volume of customers taking service from CCAs and other providers. Regardless of final methodology, equitable cost-sharing between bundled and unbundled customers ultimately means more costly unbundled rates.

Although this may ease pressure on the utilities in the near-term, cost-sharing is not expected to amount to 100% of the legacy costs (previously CPUC-approved costs) associated with serving these customers. The IOUs may remain saddled with some degree of stranded costs. Ultimately, customer rates remain the only mechanism by which utilities are able to recover their revenue requirement.

Wildfires and the New Normal for Utilities

“The New Abnormal”

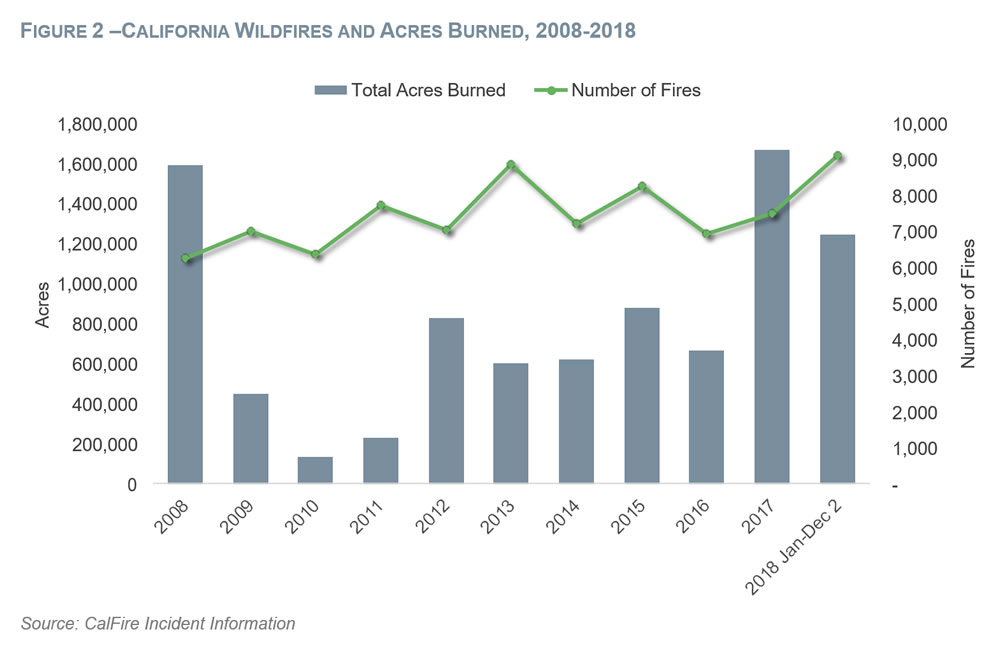

According to CalFire data, the five-year rolling average of acres burned in California has almost doubled from 2015 to 2018. The increasing frequency of extreme weather events – what Governor Brown has referred to as the “new abnormal”14 – has had significant impacts on public health, disrupted thousands of residents, and is likely to be a dominating factor in state planning and politics for the foreseeable future.

Utilities Exposed

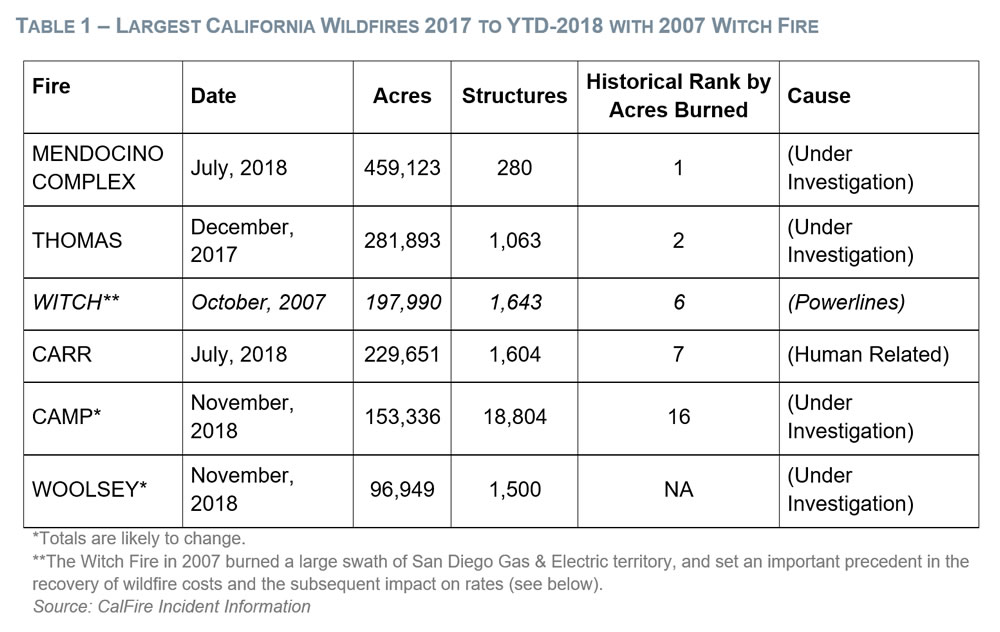

The fires of 2017 and 2018 were unprecedented in size and in the amount of damage they inflicted. Although the involvement of utility equipment has not yet been confirmed in some cases, the state’s IOUs have come under tremendous financial pressure. Immediately following Camp and Woolsey fires at the end of 2018, both PG&E and Edison International, the parent company of Southern California Edison (SCE), experienced stock price slides steeper than the declines that preceded PG&E’s 2001 bankruptcy.15 This drop in investor confidence was driven in large part by a legal construct known as “inverse condemnation”. The principle exposes California utilities to severe financial liabilities by holding them responsible for wildfire damages involving their equipment, whether or not their behavior is deemed negligent. In essence, the utilities have traditionally been on the hook for 100% of liabilities, even if they were operating within the rules implemented by the CPUC. The causes of the largest fires from 2018 are still under investigation, but both PG&E and SCE received equipment failure alerts coincident with the time and origin of the Woolsey and Camp fires.16 Although PG&E was cleared of any involvement in the 2017 Tubbs fire, the outstanding potential for liabilities from the Camp fire and dozens others are the driving factor in the company’s January bankruptcy filing. Even prior to PG&E’s recent woes, the state recognized the increasing severity of wildfires and began working to provide some degree of financial protection for utilities.

Recent Wildfire Regulations and Legislation

Following the 2017 fires, the CPUC approved memorandum accounts that grant PG&E and SCE the ability to track incremental unreimbursed wildfire liability costs. Since mid-2018, the memorandum accounts have made wildfire-related costs recoverable through rate increases upon approval by CPUC.

More significantly, the state passed SB 901 in late 2018, implementing four key changes that impact California utility customers:

- Requires the CPUC to use a financial stress test when determining allocation of costs associated with wildfire liabilities.17

- Allows investor-owned utilities to securitize wildfire liabilities through cost-recovery bonds, subject to a CPUC reasonableness review. 18

- Requires utilities to submit Wildfire Mitigation Plans (utilities to submit drafts in February 2019).19

- Established the Commission on Catastrophic Wildfire Cost and Recovery, for examination of how state policy allocates liability and compensates for fire damage.20

In 2019, the CPUC will be able to consider a broader range of factors when deciding whether costs associated with wildfires can be passed on to electric customers. Although SB 901 did not change the inverse condemnation rule, it authorizes some degree of cost recovery for liabilities. Importantly, it also mandated preventative spending by utilities recoverable through customer rates.

Bringing Electricity Customers into the Mix

The IOUs are now working to implement the CPUC’s direction to mitigate the impact of future wildfires. Wildfire prevention by the utilities spans a broad range of solutions and spending programs:21

- Prevention and emergency response

- Establishing a dedicated center to monitor wildfire risks in real time and to coordinate prevention and response efforts

- Expansion of network weather stations to enhance weather forecasting and modeling

- New and enhanced safety measures

- Expanding and accelerating vegetation clearing and safety work

- Partnering with customers in high fire-threat areas to create safe spaces between distribution lines and the trees and brush that can act as fuel for wildfires

- Refining protocols to proactively turn off electricity during extreme fire danger conditions

- Longer-term electric system hardening

- Investing in stronger, coated power lines

- Replacing wood poles with non-wood material in high-risk areas

All of these programs will drive a sustained, long-term increase in the cost to serve California customers. Moreover, California electric utilities are asking for a higher return on investment. PG&E requested a return on equity (ROE) of 12.5% in its October 2018, up from last year’s approved 10.75% ROE.22 The higher ROE request is related to the investment community’s higher perceived risk of California electric utilities. Indeed, PG&E’s credit rating was downgraded twice in 2018 prior to its bankruptcy filing.23 A utility’s cost of capital is a major driver of its cost to serve customers, and sustained increases will lead to higher customer bills for the foreseeable future.

Although the new legislation and CPUC rules are a direct response to the 2017 and 2018 fires, these cost impacts are not without precedent. In 2007, the Witch Fire in SDG&E’s territory led to significant company mitigation. A risk mitigation program implemented in 2014 is a $1 billion initiative that replaces older, overhead distribution lines in the areas deemed most at-risk for wildfires with stronger steel poles, and pays for additional technologies to make the system more resilient to harsh weather conditions.24 SDG&E’s pending 2019 General Rate Case (GRC) includes risk mitigation requests of $107.7 million, a 78% increase over 2016 recorded expenses.25 It is noteworthy that in 2018, SDG&E customers paid on average 38% more than PG&E customers and 54% more than SCE customers.26

What Comes Next

In October of 2018, the CPUC opened R. 18-10-007, to implement wildfire mitigation plans pursuant to Senate Bill 901. The rulemaking’s current schedule requests formal wildfire mitigation plans to be filed with the CPUC in February 2019. SCE recently proposed $582 million in incremental costs to address wildfire mitigation plans required by Senate

In October of 2018, the CPUC opened R. 18-10-007, to implement wildfire mitigation plans pursuant to Senate Bill 901. The rulemaking’s current schedule requests formal wildfire mitigation plans to be filed with the CPUC in February 2019. SCE recently proposed $582 million in incremental costs to address wildfire mitigation plans required by Senate

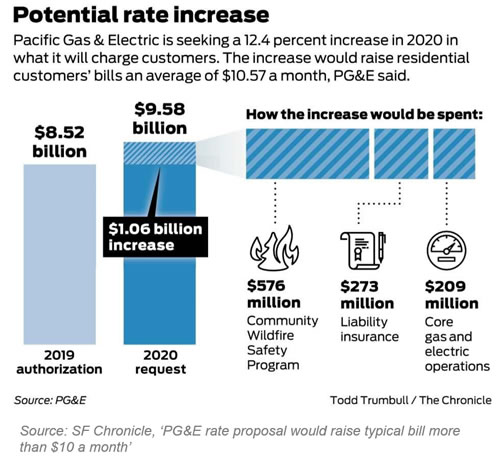

Bill 901.27 This request is only related to prevention, and does not include possible liability costs from the wildfires of 2017 or 2018, which could also be recoverable through rates, subject to CPUC review. In mid-December, PG&E made its first major request that incorporated its plans for incremental (beyond 2017 recorded costs) wildfire prevention and risk management. PG&E is proposing to invest approximately

$5 billion on risk mitigation measures between 2018 and 2022.28 The proposal accounts for a 12.4% increase in revenue requirement in 2020 from the currently- authorized 2019 amount. This massive spending request has since been overshadowed by PG&E’s bombshell filing for Chapter 11 bankruptcy on January 29th. In a press release first announcing their intent PG&E stated:

“…PG&E Board and management team have determined that initiating a Chapter 11 reorganization for both the Utility and PG&E Corporation represents the only viable option to address the Company’s responsibilities to its stakeholders.”29

It now falls to regulators, legislators, and potentially even the courts to determine who will pay for liability costs estimated to be in excess of $30 billion. These costs and their mitigation are still under investigation, and will go through a lengthy legal process guided by the recently passed SB 901, but given the sheer scale it is highly likely that at least some of the liabilities will ultimately be recovered through rates.

Regardless of the eventual outcome of PG&E’s bankruptcy proceedings, in the near term, severely constrained access to capital, higher borrowing costs, and the aforementioned wildfire prevention spending plans will all apply significant upward pressure to customer rates. Importantly for customers, this is not a trend unique to PG&E. Putting aside the liabilities specific to the most recent fires, credit downgrades, increased cost of capital, and massive wildfire prevention spending programs will impact customers of all three California IOUs, as well as municipal providers in fire-prone areas. As the state prepares for a future with more frequent destructive wildfires, so too must utilities and their ratepayers.

Conclusion

The accelerating pace of customers transitioning to unbundled service, and the staggering influx of new costs stemming from massively destructive wildfires are placing California electric utilities in an increasingly precarious financial situation. Regulators and legislators have signaled a willingness to help mitigate this financial pressure, in part by creating new mechanisms for costs to be shared with electricity customers. These changes are not simple responsive measures to a series of isolated events; rather, they represent the beginning of a new status quo for the cost to serve electric customers in California. The industry response to this new state of affairs remains to be seen, but the major decisions made recently and in coming years show that customers should reasonably expect to share the costs associated with the ongoing stabilization of California’s electricity market.

1 CPUC, California Customer Choice: An Evaluation of the Regulatory Framework Options for an Evolving Electricity Market, August 2018.

2 Public Utilities Code §331.1(a).

3 CPUC, California Customer Choice.

4https://cal-cca.org/cca-impact/, accessed December 20, 2018.

5 Ibid

6 CPUC, California Customer Choice.

7 CPUC, R. 17-06-026, Decision Modifying the Power Charge Indifference Adjustment Methodology.

8 CPUC, R. 17-06-026.

9 PG&E, Understand your energy statements, accessed December 12, 2018.

10 CPUC, CPUC Ensures Changing Electric Market is Equitable for Customers, October 11, 2018.

11 CPUC, A. 18-06-001, ERRA 2019 PG&E – Forecast, Attachment 2.

12 CPUC, A. 18-06-001, Proposed Decision, December 7, 2018.

13 CPUC, California Renewables Portfolio Standard (RPS).

14 The Sacramento Bee, Brown swings back at Trump: Climate change is propelling California’s fires, governor says, November 11, 2018.

15 Bloomberg, PG&E, Edison Plummet Most in 16 Years on Wildfire Fallout, November 12, 2018.

16 CPUC, November 2018 Wildfires, accessed December 28, 2018.

17 S&P Global Market Intelligence, Calif. wildfire costs among issues affecting utilities in newly enacted laws, September 24, 2018.

18 Ibid

19 PG&E, Advice 5419-E, Fire Risk Mitigation Memorandum Account Pursuant to Senate Bill 901.

20 SB 901, Dodd. Wildfires.

21 PG&E, Community Wildfire Safety

22 PG&E, Advice 5407-E, October 1, 2018 Transmission Owner Filling.

23 S&P Global Market Intelligence, “Wildfire risks prompt Fitch downgrade of PG&E, Pacific Gas and Electric”, November 16, 2018.

24 SDG&E, Risk Assessment Mitigation Phase Risk Mitigation Plan Climate Change Adaptation (Chapter SDG&E-14), November 30, 2016.

25 SDG&E, A.17-10-007 Exhibit: SDG&E-15-2R.

26 CPUC, 2018 SB 695 Report, p. 8.

27 Southern California Edison, SCE Proposes Grid Safety and Resiliency Program to Address the Growing Risk of Wildfires, September 10, 2018

28 CPUC, A. 18-12-009, Test Year 2020 General Rate Case Application of Pacific Gas and Electric Company.

29 PG&E, PG&E Remains Committed to Providing Safe Natural Gas and Electric Service to Customers as it Prepares to Initiate Voluntary Reorganization Cases Under Chapter 11, January 14, 2019.